Garri sold in a market in Abia State and cassava starch shipped from Vietnam to a European adhesive factory come from the same crop, yet most market overviews only ever describe one side of that picture.

The cassava market is bigger and more fractured than most single reports capture. Some analysts size it in the low billions, tracking only refined starch.

Others size it at nearly two hundred billion, counting every dish and derivative worldwide.

Neither number is wrong; they are just measuring different things.

What is consistent across every credible source is where the crop is concentrated, how it moves from root to product, and which forces are actually driving demand.

I farm cassava, process it, and sell it through Cassava Pathway, so this guide reflects both the data and what that data looks like from the production side.

Table of Contents

The Cassava Americans Import Comes From Farms Like Mine

Most of what Americans and countries like China know about cassava comes from a grocery store aisle or a health food blog.

What I bring to this guide is the other end of that supply chain.

As a cassava farmer in Nigeria, one of the world’s largest cassava-producing regions, I process the same crop that ends up in American kitchens as flour, tapioca starch, and frozen yuca.

I have never grown cassava in Florida or cooked it in a New York kitchen, but I have grown it my entire life on the farms it comes from.

That production-side perspective is what makes this guide different from every American-written article about cassava in the US.

Global Cassava Production

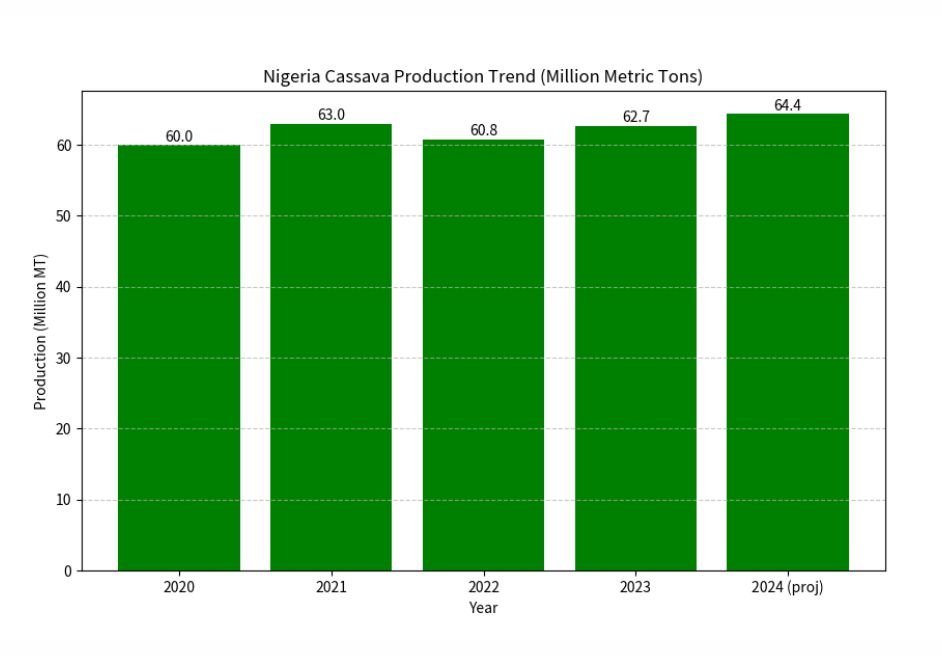

Cassava production has no single global center, since three countries account for most of it.

Nigeria, the Democratic Republic of the Congo, and Thailand together account for 42 percent of global cassava consumption, according to IndexBox’s 2026 World Cassava Market Report.

Nigeria alone processes most of its harvest into garri and fufu for domestic consumption, while Thailand’s output feeds a large export-oriented starch industry.

Ghana, Brazil, Indonesia, Cambodia, Angola, Vietnam, and Mozambique account for roughly another third of global output between them.

Read further on the top producers of cassava root in the world for the full country-by-country breakdown.

Cassava Products and Processing

Raw cassava root has almost no shelf life, so nearly every commercial value comes from what it becomes after harvest.

- Garri and fufu dominate household consumption across West Africa, sold fresh with fast turnover and thin margins.

- Cassava flour and HQCF serve the gluten-free baking market, with stricter drying and moisture standards than traditional flour.

- The cassava starch feeds the food, textile, paper, and adhesive industries as a thickener and binder, prized for being renewable and biodegradable.

- Cassava biofuel converts starch into fermentable sugars for biofuel, pharmaceutical, and beverage industries, a smaller but growing outlet for the crop.

- Dried chips and pellets serve animal feed markets and export buyers in Asia and Europe, giving processors a use for lower-grade roots.

Cassava Product Markets at a Glance

Beyond raw production, several specific cassava-derived products have grown into markets large enough to track on their own.

The global cassava starch market alone was valued at roughly 6.6 billion dollars in 2026, a figure tracked separately from the raw cassava trade entirely.

Native and modified starch, cassava pulp, biodegradable packaging, and export-grade chips each behave as distinct markets with their own buyers, pricing, and growth patterns.

Tapioca starch specifically serves food, textile, paper, and pharmaceutical buyers, and our dedicated guide to the tapioca market breaks down that demand in full.

Cassava pulp, the fibrous byproduct left after starch extraction, is finding new buyers in animal feed and biogas production rather than being discarded as waste, as covered in our guide to the cassava starch pulp market.

Native cassava starch, unmodified and minimally processed, competes directly with modified starches in food applications where a cleaner label matters more than functional performance, a distinction our native cassava starch market guide covers separately.

Cassava-based bioplastic packaging is a smaller but fast-growing market, driven by regulations phasing out single-use plastic across the EU and parts of Asia, as detailed in our posts on the market behind cassava bags and cassava packaging market trends.

International pricing for cassava chips moves largely independently of starch pricing, since chips serve animal feed and biofuel buyers rather than food or industrial manufacturers, as tracked in our international cassava chip pricing guide.

Each of these product markets deserves its own read, since lumping them together hides real differences in who buys, why, and at what price. For the root itself as a traded commodity, see our guide to cassava root in the global market.

| Product Market | Primary Buyers | What Drives It | Full Guide |

|---|---|---|---|

| Tapioca / cassava starch | Food, textile, paper, pharmaceutical manufacturers | Industrial demand for a natural, biodegradable thickener | Tapioca market |

| Native cassava starch | Clean-label food brands | Preference for minimally processed ingredients | Native starch market |

| Cassava pulp | Animal feed and biogas producers | Turning starch-extraction waste into a saleable input | Cassava pulp market |

| Bioplastic packaging | Packaging manufacturers, retailers | Regulations phasing out single-use plastic | Cassava bags |

| Export-grade chips | Animal feed and biofuel buyers | Independent pricing tied to feed and energy markets | Chip pricing guide |

| Raw cassava root | Regional and international traders | Direct commodity trade separate from processed forms | Global root market |

Market Demand by Region

Demand looks completely different depending on which region you are in.

In Africa, cassava remains primarily a food security crop, processed into garri, fufu, and flour for daily household consumption.

In Asia-Pacific, the story flips: industrial starch dominates, with the region holding roughly 58 percent of the global cassava starch market, according to Coherent Market Insights.

Vietnam and Thailand lead in industrial demand, specifically supplying starch, ethanol, and animal feed to buyers across Asia and Europe.

In the Americas, demand is smaller in volume but growing quickly, driven almost entirely by gluten-free and clean-label food trends rather than staple consumption.

North America is the fastest-growing regional market for cassava starch by share, even though Asia-Pacific remains the largest in absolute volume.

Trade and Export Opportunities

Trade in cassava runs through very different corridors depending on the product.

Vietnam exported cassava products worth over 458 million dollars in the first quarter of 2026 alone, with China buying more than 95 percent of that volume.

Thailand remains the reference market for starch pricing globally, with buyers across Asia, the Middle East, and Europe benchmarking against Bangkok FOB export offers.

The average global export price for processed cassava reached 393 dollars per ton in 2024, a 15 percent increase year over year, according to IndexBox.

Nigeria, the largest producer, still exports a smaller share of its harvest than Thailand or Vietnam, since most Nigerian cassava is consumed domestically.

Our guide on how to export cassava from Africa and our post on international cassava chip pricing cover the practical side of entering this trade.

Who Actually Processes and Trades Cassava

Most cassava content online skips a basic question: Who actually processes and trades this crop at scale?

Global agribusiness names like Cargill, Archer Daniels Midland, Ingredion, and Tate and Lyle appear repeatedly across independent market research as major cassava starch buyers and processors.

European specialists, including Emsland Group, Roquette Frères, and AVEBE, process cassava alongside other starch crops for food and industrial clients.

At the country level, Thai and Vietnamese processors dominate export-grade starch production, while Nigerian processors remain heavily oriented toward domestic garri and flour markets.

Smallholder farmers and small processors still handle most of the actual cultivation and primary processing, even where large buyers control downstream trade.

Knowing this structure matters for market entry, since the biggest opportunities for new entrants sit in aggregation and processing, not in competing with global buyers.

Cassava Market Drivers

Three separate forces are currently pulling cassava demand in new directions at once.

The gluten-free and clean-label food movement keeps expanding cassava flour and starch demand across America and Europe, well beyond its traditional markets.

Industrial demand for starch, ethanol, and biodegradable packaging continues to grow as manufacturers shift away from petroleum-based inputs.

Food security concerns keep cassava central to African agricultural policy, since it tolerates poor soil and drought better than maize or rice.

These three drivers rarely move together, which is why a farmer and a food brand can see completely different market signals at once.

Cassava Market Challenges

The same market that creates these opportunities also creates real friction for the people producing the crop.

Poor roads and limited storage remain the most persistent problems, since fresh roots spoil within days if they cannot be moved quickly to a buyer.

In my own area of Ntigha, this is not an abstract supply chain issue; it is the difference between a good harvest and a wasted one.

Price volatility follows closely behind, since cassava prices shift with seasonal supply, local demand, and competition from substitute crops like maize and yams.

Cassava mosaic disease and limited access to improved planting materials remain ongoing production risks across much of West Africa.

Policy gaps compound all of this, including Nigeria’s continued import of cassava starch despite being the world’s largest producer of the raw crop.

Our post on the challenges facing the cassava value chain covers these constraints and possible fixes in more detail.

Technological Innovations in the Cassava Market

Technology is changing each stage of this chain, though unevenly across regions.

Precision farming tools, improved disease-resistant varieties, and better drying and milling equipment are raising yields and product consistency where they reach smallholder farmers.

Digital platforms connecting farmers directly to buyers are starting to reduce the role of intermediaries in some markets, though adoption remains uneven.

Traceability systems are becoming more relevant as export buyers demand more transparency about where their cassava actually comes from.

Investment and Business Opportunities

Cassava rewards entrepreneurs willing to enter at the right stage of this chain, not just at the farm level.

Value addition, turning raw roots into flour, starch, or ethanol, consistently earns more than selling fresh roots locally.

Export-oriented processing, contract farming arrangements, and processing-as-a-service models for smallholder farmers all represent real, underexploited opportunities.

Our guides on cassava entrepreneurship and profiting from the cassava value chain go deeper into how to structure these businesses.

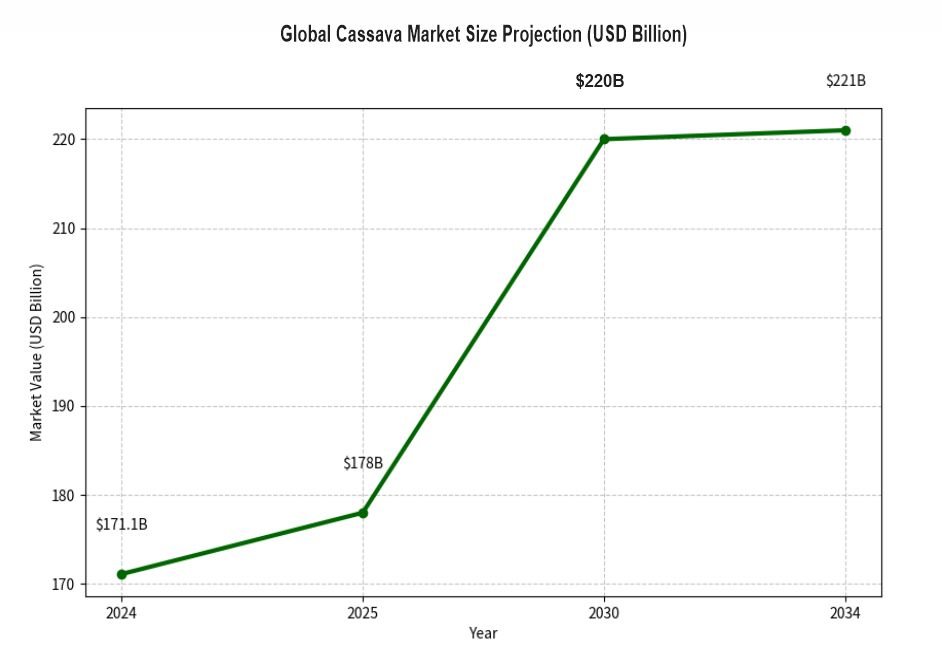

Why Cassava Market Size Estimates Vary So Widely

Search for cassava market size, and you will find numbers that disagree by two orders of magnitude, and almost no source explains why.

One widely cited report values the global cassava starch market alone at 6.6 billion dollars in 2026, tracking only refined starch products specifically.

Another values the entire cassava industry, every dish, every derivative, every country’s food consumption, at nearly 200 billion dollars for the same year.

Neither figure is dishonest; they are simply answering different questions, one about a specific commodity, the other about an entire crop’s economic footprint.

A useful rule when reading any cassava market report is to check exactly what is being measured before comparing it to a different report.

Check if the figure covers raw roots, one processed product, or the full derivative chain, since that single distinction explains most of the disagreement.

This guide deliberately avoids quoting one all-encompassing market size figure for that reason, and instead sources each specific claim to its actual scope.

Future Trends and Market Outlook

Long-term forecasts are more reliable when they stay narrow, and cassava starch specifically shows unusual agreement across independent research firms.

Multiple market reports put cassava starch growth around 7 percent annually through the early 2030s, driven mainly by gluten-free food demand and industrial starch substitution.

Asia-Pacific is expected to keep its lead in absolute volume, while North America and Europe grow fastest by percentage from a smaller starting base.

Cassava’s role in bioethanol and biodegradable packaging is widely expected to expand as manufacturers look for renewable alternatives to petroleum-based inputs.

None of this guarantees smooth growth for every farmer or processor, since regional policy, weather, and disease pressure still determine outcomes year to year.

The direction is clear even where the exact numbers are not; cassava’s footprint in industrial and health-driven markets keeps expanding, not shrinking.

Conclusion

The cassava market cannot be reduced to one number or one story. Nigeria, the DRC, and Thailand anchor global production, while Vietnam and Thailand lead industrial exports.

Africa consumes cassava as a staple, Asia processes it into starch, and America is discovering it as a gluten-free ingredient.

Each market rewards different decisions, and knowing which one you operate in matters more than any single growth projection.

I have built Cassava Pathway around that idea, one harvest at a time.

See the guides linked throughout this page to go deeper into what matters to you.

Frequently Asked Questions

What countries lead global cassava production?

Nigeria, the Democratic Republic of the Congo, and Thailand lead global cassava production, together accounting for 42 percent of world consumption, according to IndexBox market data.

Why do cassava market size estimates vary so much?

Different reports measure different scopes, raw cassava, refined starch alone, or the full derivative market, which explains most of the wide variation between published figures.

Who are the major buyers and processors of cassava?

Global agribusiness names like Cargill, ADM, Ingredion, and Tate and Lyle appear repeatedly as major cassava starch buyers, alongside large Thai and Vietnamese processors.

What is the biggest challenge facing the cassava market?

Poor transport infrastructure and storage remain the most persistent challenges, since fresh cassava roots spoil within days without quick processing or reliable market access.

What drives cassava market growth?

Cassava market growth is driven by rising demand for gluten-free foods, industrial starch, biofuels, and processed products across global food and manufacturing sectors worldwide.

Why is cassava important in global food markets?

Cassava supports global food security through products like garri, flour, starch, and fufu, while also serving gluten-free and health-focused food markets worldwide.

What are the main cassava products in demand?

High-demand cassava products include flour, starch, garri, fufu, chips, and ethanol, used in food processing, industrial manufacturing, animal feed, and export markets globally.

Chimeremeze Emeh

Chimeremeze Emeh is a tropical crop farmer and chemical engineer from Ntigha, Isiala Ngwa North LGA, Abia State, Eastern Nigeria, specializing in cassava and palm oil, with over 30 years of hands-on experience growing, harvesting, and processing cassava. He grows TMS series, TME 419, and local traditional varieties on his own farms and operates a small-scale cassava flour and starch production business through Cassava Pathway, which he founded as a CAMA-registered agribusiness in 2024. He is also the founder of Palm Oil Pathway, where he applies the same tropical farming expertise. His farms are located in Ntigha, Abia State.